Authored by: Vikram Gosain and Meenu Grover

The global conversation around obesity is undergoing a seismic shift. What was once considered a lifestyle issue is now being reframed as a chronic, relapsing disease with far-reaching health and economic implications. At the heart of this transformation are GLP-1-based therapies, a class of drugs that has rapidly moved from diabetes treatment into the center stage of obesity care and beyond.

This convergence of breakthrough science, evolving policy, and surging patient demand has created a rare and complex inflection point. For biopharma leaders, the critical question is whether to lead, adapt, or play catch-up.

In this latest insight, we’re analyzing what it takes to compete and win. We explore the market’s dynamic reshaping, the key macro and micro drivers fueling its exponential growth, and the strategic differentiation required for a crowded pipeline. We also cover the critical commercial considerations and the strategic implications of this transformation for all stakeholders, including biopharma, payers, providers, and investors.

Reshaping the Obesity Market Landscape

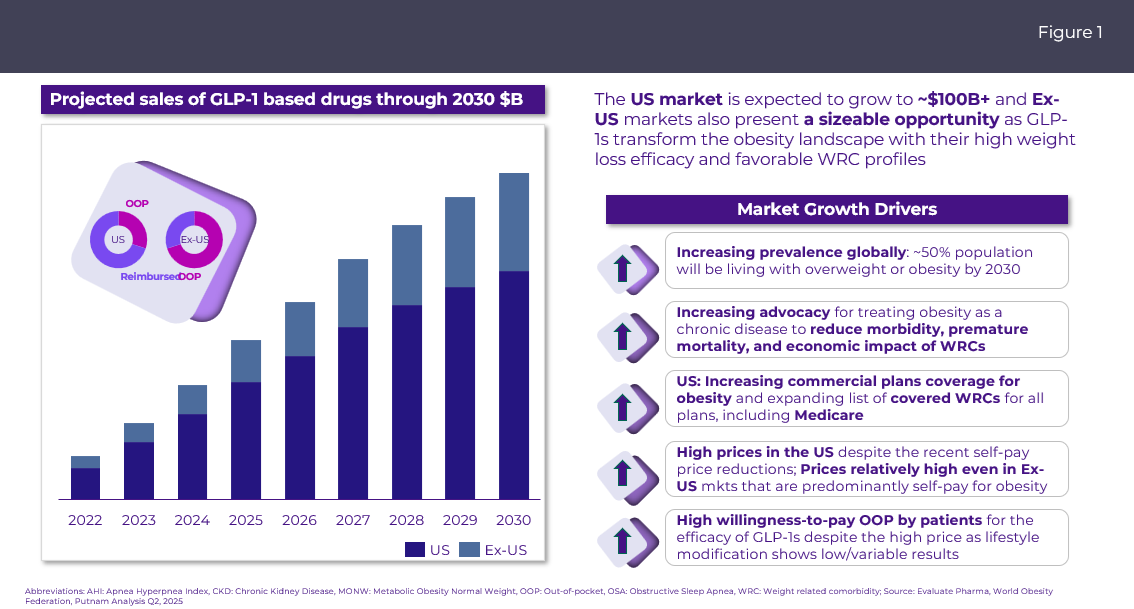

GLP-1s, including widely recognized brand names Wegovy, Mounjaro, and Zepbound, have demonstrated profound weight-loss efficacy, often in the range of 15–20% and are set to become the largest-selling drug class globally. The U.S. obesity market alone is expected to exceed $100 billion by 2030, and ex-U.S. markets are also heating up rapidly.[1]

Fig 1: Obesity market is projected to grow

exponentially in the coming years

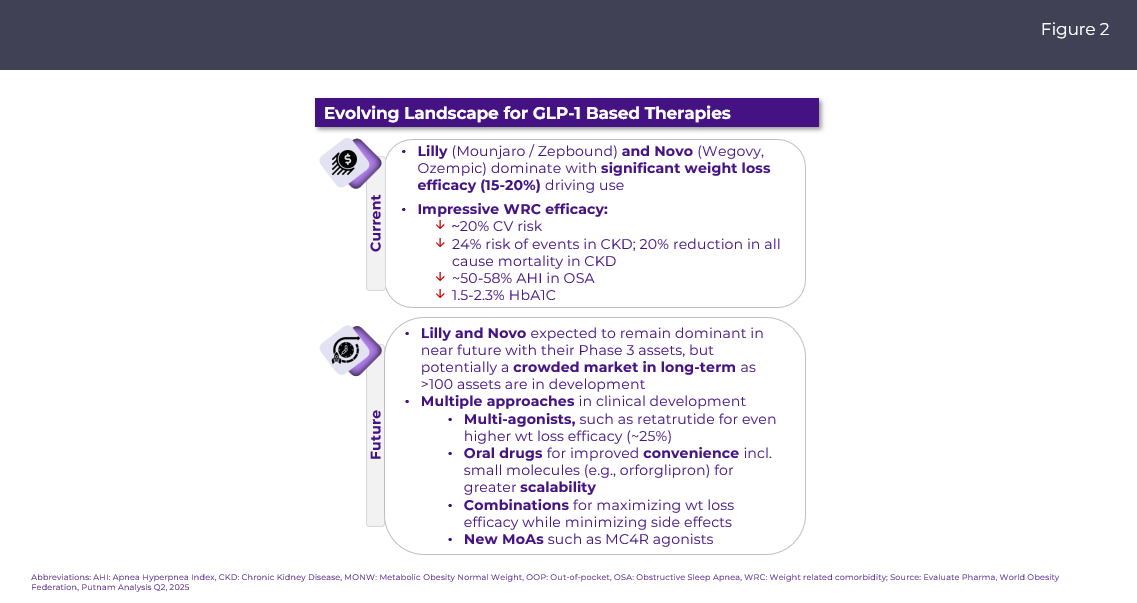

What is now a highly consolidated market dominated by Lilly and Novo Nordisk is poised to become increasingly competitive and complex. More than 100 assets are currently in development, targeting novel mechanisms of action, combination therapies, and oral formulations[2].

What’s Fueling Market Momentum?

Several macro and micro-level drivers are driving this obesity care revolution:

- Rising Prevalence: By 2030, nearly half the world’s population will be living with overweight or obesity, an alarming epidemiological trend that brings public health systems to a tipping point.

- Recognition of Healthcare Burden: There is an ever-increasing awareness that treating obesity results in meaningful improvement in cardiovascular outcomes and lowers the risk of developing multiple related cardiometabolic diseases including Type 2 Diabetes Mellitus (T2DM), chronic kidney disease (CKD), heart failure, fatty liver or MASH, obstructive sleep apnea (OSA), and peripheral arterial disease (PAD), moving the needle beyond aesthetics and towards total health improvement.

- Growing Advocacy: Medical and patient advocacy groups are pushing for obesity to be treated as a chronic condition, not a cosmetic issue, reinforcing the need for long-term, reimbursed care pathways.

- Patients’ Willingness to Pay: Despite high prices and the need for chronic use, patients have shown strong willingness to pay out-of-pocket, signaling deep consumer demand.

- Access Evolution: Until now, Medicare coverage was limited to weight-related comorbidities (WRCs) such as type 2 diabetes, CV risk reduction, and obstructive sleep apnea. That changed in November 2025, when Novo and Lilly announced an agreement with the White House to significantly drop prices for self-pay patients and extension of Medicare coverage for weight loss starting April 2026. This landmark policy announcement will reshape access, pricing, and profitability dynamics for both existing therapies and pipeline assets.

- Expanding Prescriber Universe: As GLP-1–based therapies gain additional indications and real-world experience builds, comfort among GPs in prescribing GLP-1s is likely to rise. As a result, prescribing is expected to continue to expand beyond specialists, accelerating adoption.

- A Rich R&D Pipeline: As companies continue to develop differentiated therapies with added advantages, the eligible patient population will keep growing. With several mechanisms, modalities, clinical needs, and routes of administration in development, the landscape is promising to become much more complex.

A Crowded Pipeline Means Strategic Differentiation Is Critical

With over 100 assets in clinical development, ranging from multi-agonists like retatrutide (with potential for ~25% weight loss) to oral small molecules like orforglipron, the battle for clinical and commercial leadership will be intense[3]. Players must differentiate not just on efficacy, but also on safety and tolerability, and convenience of use (e.g., oral vs injectable or weekly vs. monthly injections). Carefully selecting WRCs as follow-on/lead indications to gain reimbursement across markets where weight loss is unlikely to get covered, developing well thought out go-to-market strategy including direct-to-consumer and digital health models, and ensuring there is adequate manufacturing capacity to meet demand are also critical to success.

Fig 2: Evolving Competitive Landscape in

GLP-1 Based Obesity Medications

Abbreviations: AHI: Apnea Hyperpnea Index, CKD: Chronic Kidney Disease, MONW: Metabolic Obesity Normal Weight, OOP: Out-of-pocket, OSA: Obstructive Sleep Apnea, WRC: Weight- related comorbidity; Source: Evaluate Pharma, World Obesity Federation, Putnam Analysis Q2, 2025

Unmet Needs and Potential Differentiation Levers

Despite extraordinary promise, there are still unmet needs that biopharma companies can target to address:

GI Tolerability

The most common GI adverse events (nausea, vomiting, and diarrhea) often lead to therapy discontinuation. This, in turn, compromises efficacy and limits long-term adherence.

Muscle Loss

While patients lose fat, they often lose muscle mass too. This can result in sarcopenic obesity, particularly in older or frail populations, and raises new questions about treatment sustainability.

Further Improved and Durable Response

For patients with very high BMI, there is a critical need for new MoAs that provide improved efficacy – approaching or surpassing the benchmarks set by bariatric surgery (25–30% weight loss), either as a single agent or as a combination approach. Further, once patients achieve their desired weight, therapies that are safer, cheaper, and/or more convenient to administer may be needed to help sustain the durability of the response.

Titration Complexities

Slow titration, while necessary to reduce side effects, delays the onset of maximum efficacy. Therapies with faster or no titration could improve patient and provider experience.

Personalization of Treatment to BMI and ORC

Patient heterogeneity, including metabolically obese normal weight (MONW) individuals, patients with severe obesity (BMI ≥40), and sarcopenic elderly populations poses challenges for standardized interventions. As precision medicine tools evolve, it may be possible to tailor safe, effective, and durable obesity interventions for these diverse subgroups.

Device

In the US, Wegovy is available as single-dose autoinjector for both reimbursed and self-pay users, while Zepbound offers vials for self-pay and higher-priced autoinjectors for reimbursed segments. Outside the US, both provide flexible multi-dose pens, which Lilly will now be offering for Zepbound self-pay patients in the US as well. Balancing manufacturing scalability, cost, and patient convenience will be key to future device strategy success.

Commercial Considerations

Expanding Access

Unlike most therapy areas, the obesity market requires viewing patients as both consumers and payers, particularly in self-pay geographies and segments. Understanding how patients weigh price, product attributes, and personal goals is essential to unlocking adoption and access. Broadening access through effective patient support programs can be a key enabler in such markets.

Cross-Indication Pricing Implications

With GLP-1 therapies spanning multiple indications, cross-indication pricing poses a strategic challenge. For example, initial pricing for T2D may limit flexibility for higher-value uses like MASH. Manufacturers must strike a delicate balance between access, value perception, and sustaining profitability in the context of reimbursement constraints.

Navigating the Impending Generics Entry

Wegovy generics expected between 2026–2032 will likely reshape the market, particularly given the large self-pay, cost-sensitive patient base.

Well-crafted Go-to-Market strategy

With a large self-pay market, the need for differentiated direct-to-consumer engagement models will become more prevalent as a distinct yet complementary approach to traditional payer-driven models.

Strategic Implications for Stakeholders

For Biopharma and Biotech

Strategic decision-making is more critical than ever. Companies must evaluate whether to deepen investments in GLP-1 analog follow-ons, pivot towards innovative MoAs, or lead in combination therapies. Adjacent indications such as sarcopenia, metabolic syndrome, and MAFLD represent significant growth opportunities, provided they are thoughtfully integrated into the overall portfolio strategy.

For Payers and Policymakers

As voices for coverage grow stronger, there is a pressing need to move beyond traditional paradigms and incorporate broader value assessments. Specifically, the long-term health and economic benefits of preventing chronic conditions must be factored into coverage decisions while also balancing the budget impact. For commercial plans in the US, there will be an increasing pressure to follow Medicare’s lead and cover obesity more broadly, which will require careful evaluation of budget impact in the short- and long-term.

For Providers

Obesity management will increasingly extend beyond broad lifestyle modification advice or even pharmacologic intervention to encompass long-term weight maintenance and patient education on medication discontinuation and the potential for weight rebound. Providers must be prepared to guide patients through this evolving continuum of care, including maneuvering their way around affordability and access.

For Investors

The obesity market is no longer speculative – it’s proven, competitive, and growing. While clinical innovation remains important, investors must evaluate not just scientific differentiation, but also commercial execution, payer alignment, and scalability.

Looking Ahead: Are you Strategically Positioned?

The leaders of tomorrow recognize the complexity of obesity not just as a disease, but as a multifactorial challenge requiring integrated, interdisciplinary solutions. Now the center of the healthcare agenda, this transformation drives a race to innovate, scale, and democratize care. While biopharma must strategically choose between GLP-1 follow-ons, innovative MoAs, or combination therapies, payers must justify broader coverage by factoring in the long-term economic benefits of prevention. As providers adapt to managing long-term weight maintenance and patient education on affordability, investors must prioritize commercial execution, payer alignment, and scalability. The market’s early-stage revolution will also create significant ripple effects across adjacent sectors, including digital health, nutrition, and cardiovascular care.

At Putnam, and across our Inizio connected capabilities, we help clients across the life sciences spectrum navigate this fast-evolving landscape. Whether you’re defining your pipeline strategy, evaluating launch scenarios, designing access models, or building long-term value across the obesity ecosystem, we bring the insights and rigor needed to lead.

Let’s talk about how your organization can successfully position itself for impact and growth in the rapidly transforming obesity care ecosystem. Contact us here.